When it comes to the security of the health of employees, the government makes its best efforts to secure their rights. So, The Patient Protection and Affordable Care Act added section 6055 and 6056 to the Internal Revenue Service in 2014 which states that both the insurers and health insurance providers have to provide information about credible health insurance provided to every full time working employees. These first came into effect from the year 2015 but fully effective from 2016.

- As per section 6055 and 6056, any person providing minimum essential coverage to an individual and health insurance issuers, and applicable large employers have to report the information to the government respectively.

- The providers must report the following information to the IRS:

- Name, address and Employer Identification Number of the employer.

- Name and Taxpayer Identification Number of the employees covered under the policy.

- Name, address and Taxpayer Identification Number of each responsible individual or date of birth in case of non-availability of TIN. But once the TIN is received, it has to be provided to the IRS.

- Forms to be filed to the IRS are given below:

- 1095A– This will be used by the Health Care Exchanges and web-based health insurance marketplaces to provide the information about each individual covered under “Qualified Health Plans”. It shall be submitted to the Department of Health and Human Services who will inform it to the IRS. It shall include the coverage level, policy amount and other related information.

- 1095B– This form is submitted to the individual covered under the policy of the Health insurance Provider containing information about the coverage provided, the period of coverage and the insurer including each dependant.

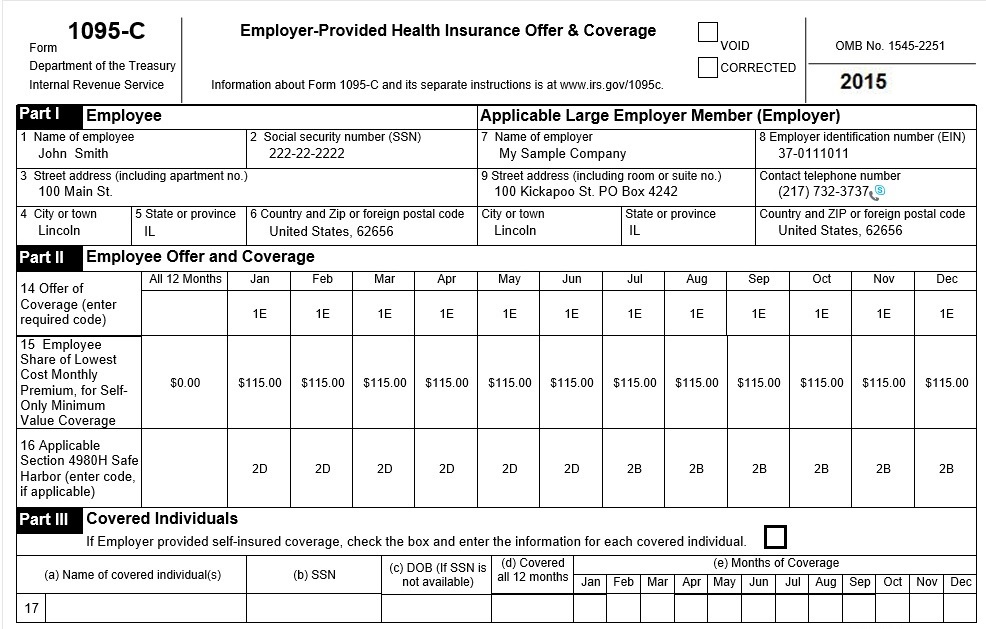

- 1095C– As per section 6056, applicable large employers has to furnish the information about each employee covered under this scheme under the form number 1095C reporting requirements. They shall furnish the type of coverage provided, identification information of each employee and its dependants.

- 1094B and 1094C– These forms are used to furnish the coverage information to IRS by Health Insurance Providers and Applicable Large Employers respectively.

- The above-listed forms are to be submitted to IRS by both the parties annually not later than 28 February and can be extended to 31 March, if submitted electronically, of the year following the calendar year in which the minimum essential coverage is provided to the individual. Employers can request for 30 days extension by providing a suitable reason for not submitting on time.

- If an employer fails or delays to submit information under section 655 or 656 to the IRS or responsible individual within the time period allowed, fines and penalties can be imposed on him as per section 6721 and 6722. But, the penalties may be reduced if any corrective action is taken towards this or there is a suitable reason to justify this mistake. The employer is charged indexed penalty up to a calendar year maximum. It can be doubled if it is not submitted to IRS and responsible individual.

All the employers covered under these sections are strongly encouraged to collect all the information correctly and furnish all the required information to the interested parties within the time given to avoid any penalties or fine.